Learn about India’s Payment Systems — UPI, RuPay, and Central Bank Digital Currency (CBDC or Digital Rupee). Updated, concise, and UPSC-relevant notes for Economy GS Paper 3 and Prelims.

Introduction:

India’s financial ecosystem has undergone a revolutionary transformation in recent years, driven by digital innovation and government-led initiatives promoting cashless transactions. Understanding payment systems like UPI, RuPay, and the Digital Rupee (CBDC) is essential for UPSC aspirants, especially under topics related to Indian Economy, Financial Inclusion, and Digital Governance.

1. What are Payment Systems?

A payment system is a mechanism that enables the transfer of money between individuals, businesses, and governments.

It includes instruments, procedures, and interbank arrangements to facilitate monetary transactions efficiently and securely.

Regulatory Authority:

The Reserve Bank of India (RBI) and the National Payments Corporation of India (NPCI) are the key regulators and operators of India’s payment systems.

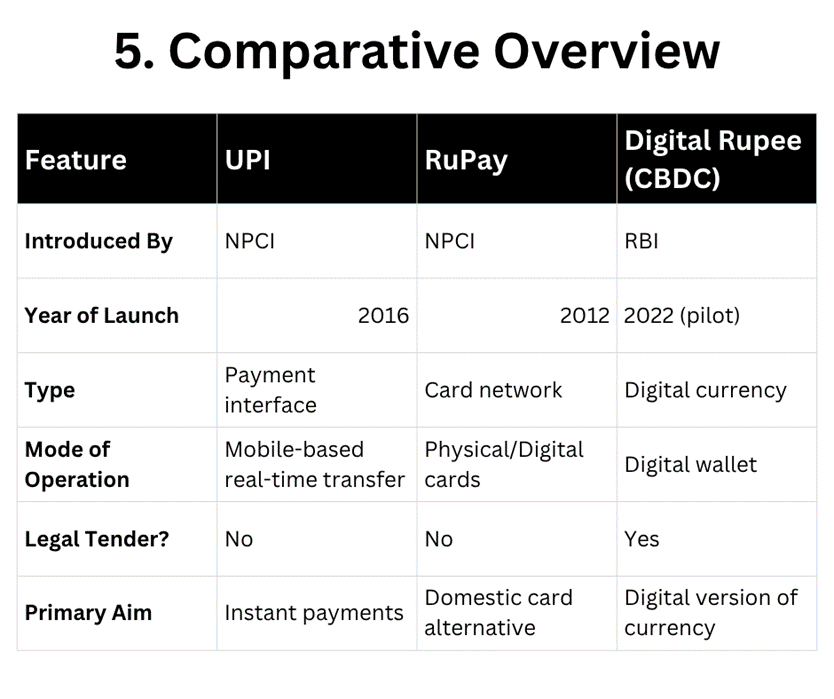

2. Unified Payments Interface (UPI)

Overview:

- Launched: April 2016 by NPCI

- Objective: Seamless fund transfer between bank accounts through mobile devices in real time.

- Tagline: “One App for All Payments”

Key Features:

- Instant fund transfer, 24×7

- Operates via Virtual Payment Address (VPA) – no need to share bank details

- Supports peer-to-peer (P2P) and peer-to-merchant (P2M) payments

- Integrated with BHIM, Google Pay, PhonePe, Paytm, etc.

-

Advantages:

- Promotes Digital India and financial inclusion

- Reduces dependence on cash

- Facilitates interoperability among banks and apps

-

Recent Developments (as of 2025):

- UPI Lite: Enables small offline payments without internet

- UPI for NRIs: Linked to international phone numbers in select countries

- UPI-PayNow Linkage: Cross-border payments between India and Singapore

-

UPSC Relevance:

- GS Paper 3 – Indian Economy (Digital Payments)

- Prelims – NPCI, RBI initiatives, and current affairs

-

3. RuPay Card

Overview:

- Launched: 2012 by NPCI

- Objective: Indigenous alternative to international card networks like Visa and Mastercard

- Meaning: “RuPay” = Rupee + Payment

-

Types of RuPay Cards:

- Debit Cards

- Credit Cards

- Prepaid Cards

-

Features:

- Lower transaction costs

- Secure domestic transactions

- Accepted globally (via partnerships with Discover and JCB)

- Linked with Jan Dhan Yojana – every beneficiary receives a RuPay card

- Benefits:

-

Encourages financial inclusion

- Strengthens India’s payment sovereignty

- Promotes the Make in India initiative

-

UPSC Relevance:

- GS Paper 2 – Government Schemes (Financial Inclusion)

- GS Paper 3 – Economic Growth & Digital Economy

-

4. Central Bank Digital Currency (CBDC) – Digital Rupee

What is CBDC?

A Central Bank Digital Currency (CBDC) is the digital form of fiat currency issued by the Reserve Bank of India (RBI).

It is a legal tender, equivalent to paper currency, but exists only in electronic form.Types of CBDC (as per RBI):

- Retail CBDC (e₹-R): For individuals and small businesses

- Wholesale CBDC (e₹-W): For financial institutions and interbank settlements

-

Launch Timeline:

- Pilot launched: November 2022

- Issuing Authority: Reserve Bank of India

-

Features:

- Legal tender backed by RBI

- Available via digital wallets issued by banks

- Works both online and offline (pilot phase)

- Enhances transparency and traceability in transactions

-

Benefits:

- Reduces cost of currency management

- Boosts financial inclusion

- Supports India’s move toward a cashless economy

- Enhances efficiency in cross-border payments

-

Challenges:

- Objective: Reduce currency printing cost, promote efficiency in transactions

-

- Cybersecurity risks

- Privacy concerns

- Need for digital literacy and robust infrastructure

-

UPSC Relevance:

- GS Paper 3 – Monetary Policy & Financial Innovation

- Essay Paper – Technology and Economy Interface

6. Way Forward:

India’s journey toward a digital economy is anchored in secure, inclusive, and innovative payment systems.

The integration of UPI, RuPay, and CBDC is shaping India’s position as a global leader in fintech innovation.

For UPSC aspirants, understanding these systems reflects awareness of the intersection between technology, economy, and governance — a crucial area in both Prelims and Mains.

Conclusion:

From UPI’s real-time transfers to RuPay’s indigenous card network and the futuristic Digital Rupee, India’s payment architecture demonstrates its vision of becoming a digitally empowered economy.

For UPSC aspirants, these topics not only aid in understanding the economic reforms but also provide rich material for GS Paper 3, Essays, and Interviews.