Introduction

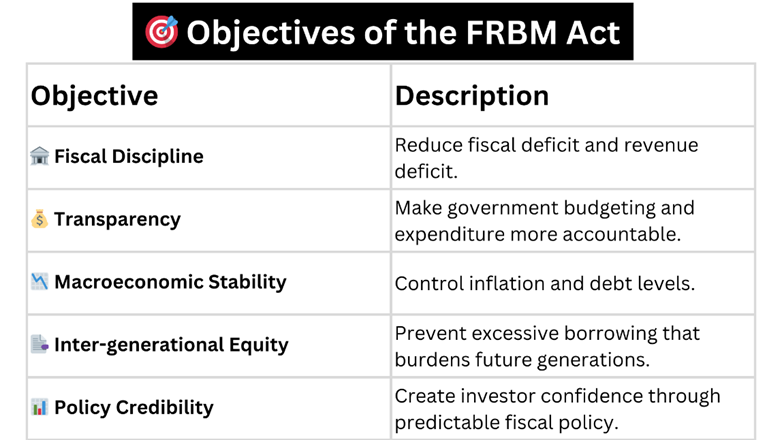

Fiscal discipline is the backbone of a stable economy. To ensure responsible budgeting and prevent fiscal slippage, India enacted the Fiscal Responsibility and Budget Management (FRBM) Act, 2003.

This landmark legislation aims to institutionalize financial discipline, reduce fiscal deficit, and enhance transparency in the management of public funds.

Background of the FRBM Act

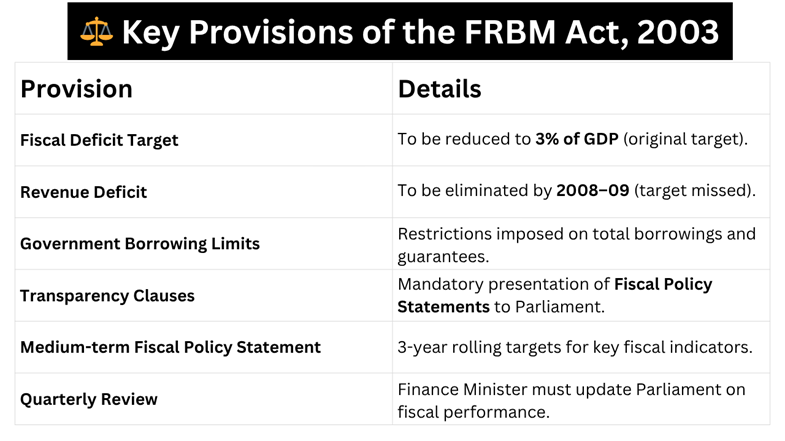

- The FRBM Act, 2003 was enacted by the Parliament of India and came into force on July 5, 2004.

- It was introduced by Finance Minister Yashwant Sinha during Atal Bihari Vajpayee’s government.

- Objective: To bring fiscal discipline at both Central and State levels, ensuring inter-generational equity and macroeconomic stability.

Important Amendments to the FRBM Act

1️⃣ 2012 Amendment

- Introduced the concept of Effective Revenue Deficit (ERD) = Revenue Deficit – Grants for Capital Creation.

- Added a Medium-Term Expenditure Framework (MTEF) statement to be presented to Parliament.

2️⃣ 2015 Amendment

- Linked fiscal consolidation with the recommendations of the 14th Finance Commission.

- Focus shifted toward debt sustainability.

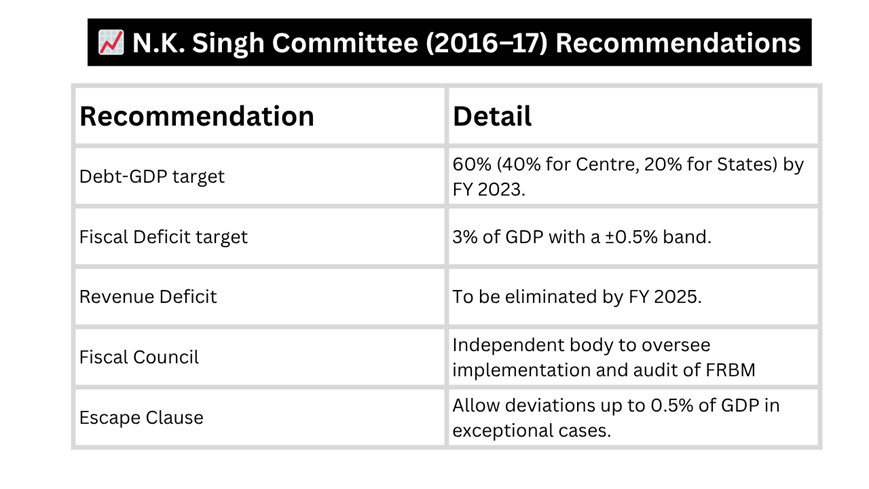

3️⃣ 2018 Amendment (Based on N.K. Singh Committee Report, 2017)

- Replaced fiscal deficit and revenue deficit targets with a Debt-to-GDP Ratio framework.

- Introduced “Escape Clauses” — allowing temporary deviation from fiscal targets under specific conditions.

- Set new medium-term targets:

- Fiscal Deficit: 3% of GDP by March 2021

- Central Government Debt: To be reduced to 40% of GDP

- General Government Debt: To be reduced to 60% of GDP

Escape Clauses under FRBM Act (Post-2018)

The Central Government may deviate from annual fiscal targets in the following cases:

- National security or natural calamity.

- Structural reforms with fiscal implications.

- Decline in real output growth by 3% or more.

- Other exceptional circumstances approved by Parliament.

Example: The government invoked the escape clause during COVID-19 (2020) to allow higher borrowing and fiscal deficit (up to 9.5% of GDP).

UPSC Prelims Practice Question

Q. Consider the following statements about the Fiscal Responsibility and Budget Management (FRBM) Act, 2003:

- It aims to eliminate revenue deficit and reduce fiscal deficit to 3% of GDP.

- It provides for the establishment of an independent Fiscal Council.

- The Act allows deviation from fiscal targets under specified conditions.

Which of the statements given above is/are correct?

(a) 1 and 2 only

(b) 1 and 3 only

(c) 2 and 3 only

(d) 1, 2 and 3

✅ Answer: (b) 1 and 3 only

Challenges in Implementation

- High subsidy burden and populist spending.

- Slippage in disinvestment targets.

- Revenue shortfall due to slow growth.

- Lack of an independent fiscal council.

COVID-19 and global crises increasing debt burden.

Conclusion

The FRBM Act represents India’s commitment to sound fiscal governance and macroeconomic stability. However, the real test lies in balancing fiscal prudence with developmental expenditure.

As India eyes a $5 trillion economy, fiscal responsibility must evolve with flexibility — ensuring growth without compromising discipline.

Related articles : Fiscal Policy of India – Meaning, Objectives, and Instruments | UPSC Notes

Budget Deficits Explained: Fiscal, Revenue, and Primary Deficit – Complete Notes for UPSC CSE

Payment Systems in India: UPI, RuPay, and Digital Rupee CBDC – Key Notes for UPSC CSE Preparation